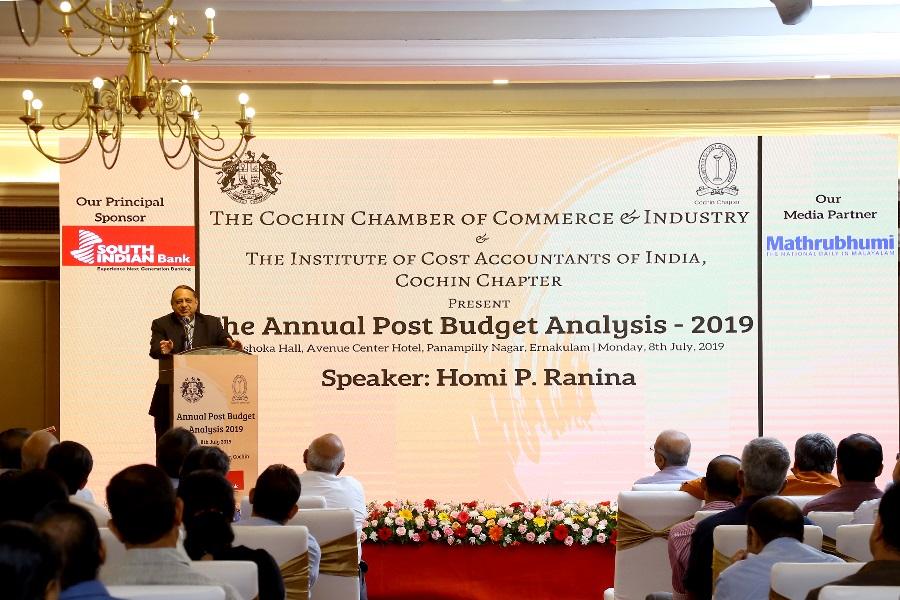

Gist of the speech delivered by Mr. H. P. Ranina, noted tax expert, on “Union Budget, 2019-20” under the auspices of the Cochin Chamber of Commerce on Monday 8th July, 2019

The maiden budget of Ms. Nirmala Sitaraman lays down the road map for a strong and vibrant economy. This is despite the gloomy global economic scenario and the lower projected growth rate of 6.8% for the Indian economy during 2018-19. The success of the second term of the Modi Government will be tested by the outcomes rather than the outlays proposed in this year’s budget documents.

The Finance Minister has presented her budget proposals with a degree of caution and trepidation. Her exercise at creating a fine balance between the need for fiscal consolidation and promoting growth has ensured that no populist measures are announced. She needs to be complimented for having brought down the fiscal deficit to 3.3% of GDP for fiscal year 2019-20.

Fiscal consolidation is the only path available for restoring credibility in the Indian economy.

The Government has shown its sincerity and commitment to tackle the problems facing the jobless youth. The emphasis is to encourage young job seekers to become job creators. Promoting employment opportunities in the textile, retail, food processing and construction sectors has been a critical need which has been partially addressed by the Government. Not enough has been done to make labour laws flexible and in line with modern day trends prevailing in developing countries which have a growing young population as in India.

To promote ease of doing business, the Government has successfully launched an e-Biz portal which will integrate 14 regulatory permissions. This will make it possible to start a new business without obtaining prior approvals, so long as such start-ups are in conformity with guidelines and criteria. Exemption of start-ups from the angel tax is a step in the right direction. The objective is to encourage young entrepreneurs to create value out of ideas and initiatives.

Affordable housing has been given the right impetus which will also give a boost to employment creation, given the high degree of forward and backward linkages with other segments of the economy. The higher tax break in respect of interest paid upto Rs. 3.5 lakhs on loans taken for purchase of houses valued at Rs 45 lakhs or less will help young people to settle down and at the same time give a boost to the construction industry.

To drive the momentum on private consumption, the budget proposals focus on ways to increase rural income which, in turn, will promote rural demand. To ensure higher income in the hands of agriculturists, involvement of the corporate sector has been suggested which would enable use of advance technology in key areas, like micro-irrigation, crop care, advanced seeds and selection of the right crop having regard to the soil conditions. Agri reforms are sought to be introduced by encouraging adoption of the Model Agricultural Land Leasing Act, 2016 to facilitate consolidation of land.

Between July and September this year, the Government is proposing to invest Rs.15,000 crore in the Jal Shakti Abhiyan scheme which will cover 200,000 works to be taken up for water conservation in nearly 1,100 water stressed blocks. The employment guarantee scheme which mandates that 60% of its expenditure is to be incurred on national resource management, has set a target for construction of farm ponds, rainwater harvesting, re-use of water and intensive afforestation. The Government is determined to provide piped drinking water to every household by 2024.

As a key measure of labour reform, the Government has introduced the Code on Wages Bill which will make minimum wages applicable in both formal and informal sectors and make it mandatory for payment of wages directly into the bank account of employees. Under this legislation, the Central/State Governments will determine the factors for fixing the minimum wages for different categories of employees based on their skill, the arduous nature of the work, geographical location and other critical and special aspects.

Personal income tax rates have been left unchanged and those who have taxable income upto Rs. 5 lakhs will not have to pay tax at all. Increase in the rate of surcharge on those having more than Rs. 2 crores of taxable income will affect just a few tax payers, less than 50,000 out of a population of 1.3 billion. Citizens are greatly relieved that wealth tax and inheritance tax are not proposed to be introduced as was feared.

Tax on companies having turnover of upto Rs. 400 crores has been reduced to 25% which will now be applicable to 99.7% of the corporate sector. The capital gains tax structure has not been tinkered with. Gifts made by residents to non-residents will be taxable in India in the hands of the latter unless such non-residents are relatives as defined in the Income tax Act. If payment made to a contractor or professional exceeds Rs. 50 lakhs in a financial year, tax will be deductible at source by an individual who pays such amount.

Foreign institutional investors and other market players have invested more than USD 11 billion in Indian equities in the past few months primarily on ground of political stability and the present Government’s commitment for pushing economic reforms. This is also due to the fact that other economies like China are facing uncertainty with the trade war with the U.S. Government looming large. Foreign investors are also banking on the fact that interest rates will keep coming down in India and the domestic demand will show a healthy trend in the coming year.

The Budget proposals are replete with big ideas in social security, education and foreign direct investment. Policy credibility is a precious commodity in these turbulent global times. If consumption demand picks up as a result of additional public expenditure and a normal monsoon this season, India would be on the growth path with a 7.2% increase in GDP in fiscal year 2019-20 as against 6.8% in 2018-19. This will lay the foundation for a strong and vibrant economy which is expected to grow to US$ 5 trillion by 2023, making it the third largest economy in the world.